Jobs report exaggerated the increase in U.S. hiring in 2023

The U.S. added a surprisingly large 2.7 million new jobs in 2023 as the economy defied a widely forecasted recession, but monthly increases were exaggerated by pandemic-era distortions in how they are counted.

Make no mistake. The U.S. labor market is historically strong. Good workers are hard to find and companies have to pay more to attract and keep them. The unemployment rate sits at a very low 3.7%.

Yet the official U.S. employment reports chronically overstated how many jobs were created each month in 2023, potentially misleading Wall Street, the Federal Reserve and Washington lawmakers about the true strength of the economy.

From January to October, the government initially overestimated job growth in nine of the 10 months. Eventually the employment gains were reduced by an average of 55,000 a month, an unusually large change.

Take last June as an extreme example. The government initially said a robust 209,000 new jobs were created before marking its finally estimate down to a tepid 105,000 two months later.

At the time, the stronger-than-expected report may have kept the Federal Reserve primed to keep raising interest rates amid worries that a hot labor market was keeping too much upward pressure on inflation.

What’s going on?

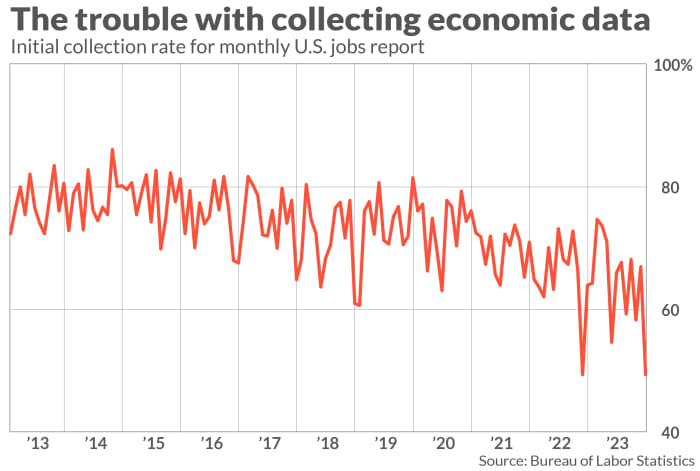

Some economists blame the low level of response by businesses surveyed by the Bureau of Labor Statistics to determine how many jobs are created each month.

“Low response rates to the BLS’s monthly establishment survey have been an issue since the onset of pandemic and continue to diminish the reliability of the initial estimate of job growth in any given month,” contended Richard Moody, chief economist of Regions Financial.

Take the December jobs report, when the government reported a bigger-than-expected 216,000 increase in new jobs.

The so-called collection rate — the share of businesses that responded — matched a 32-year low of 49.4%.

By contrast, the average collection rate for the preliminary jobs report was around 73% before the pandemic.

The BLS says its own research shows no correlation between a low initial collection rate and large changes between preliminary and final estimates of monthly job gains.

“The large downward revisions in 2023 are not necessarily the result of a lower collection rate,” said BLS economist Purva Desai.

The agency said its trying new approaches to try to get more businesses to respond in a timely manner. The key is “timely.”

Most businesses, in fact, do turn in their employment surveys eventually. The collection rate after the third and final estimate of a monthly jobs report is stable at 90%-plus.

The big question is why so many respond so late.

Survey fatigue is one reason. The pandemic has also made it harder for the BLS to get in touch with businesses to get them to enroll in the survey. And sometimes the people at the companies who respond to the survey work from home and do not respond as quickly.

Beyond that, one one seems to know.

“We also continue to boost efforts to increase initiation and collection by offering respondents easier and more flexible ways to enroll and report their employment data,” Desai said.

In the meantime, investors and policymakers should treat the initial jobs report and other economic reports with caution, Moody and other economists say. They all suffer from the same problem to varying degrees, making the quality of the data suspect at first glance.

“I’ll be watching to see how the 2024 estimates fare,” Moody said.